Inventory Expansion and Market Rebalancing

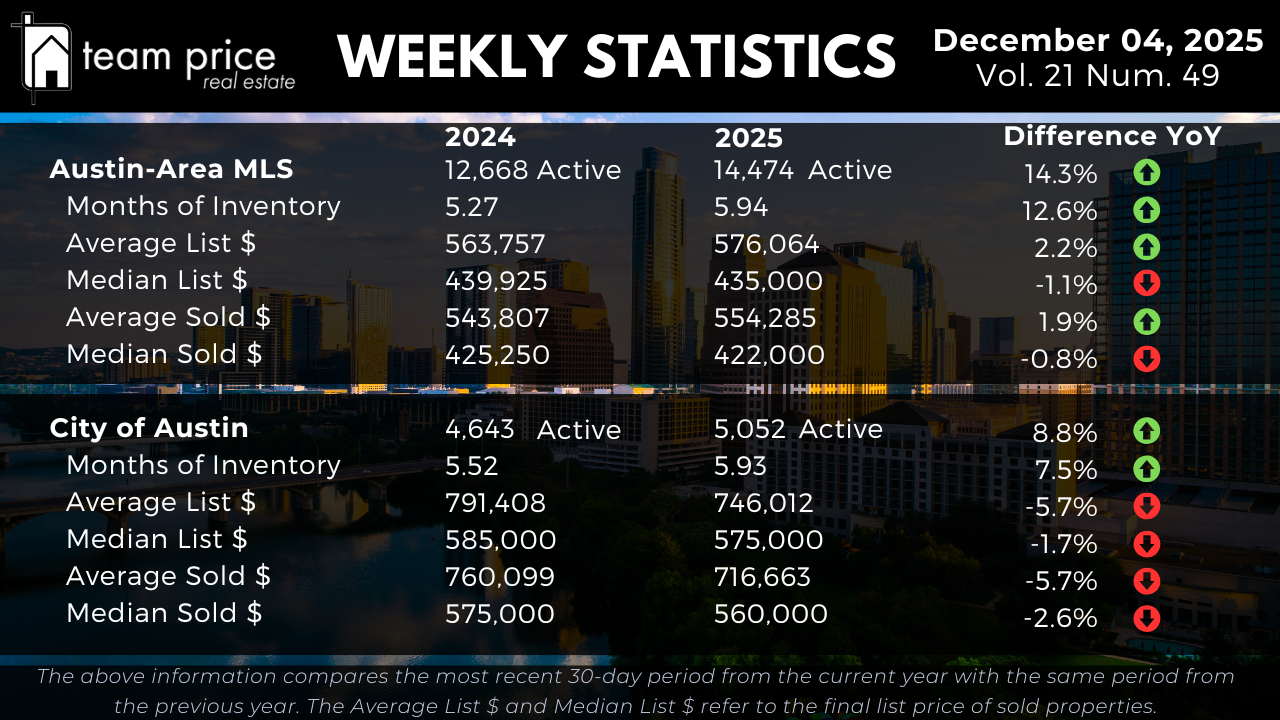

Inventory continues to expand across the Austin housing market as supply grows faster than buyer demand absorbs it. Active listings in the Austin-Area MLS rose from 12,668 last year to 14,474 today, a 14.3% increase. Months of Inventory climbed from 5.27 to 5.94, a 12.6% rise that represents a 1.1× expansion in available supply. This level of inventory places the region firmly in a supply-led environment, where homes take longer to attract offers and buyers have more leverage in negotiations.

Inside the City of Austin, inventory growth is more moderate but still meaningful. Active listings increased 8.8%, rising from 4,643 to 5,052. Months of Inventory moved from 5.52 to 5.93, a 7.5% increase that aligns closely with the metro-level trend. Both city and suburban markets are following the same trajectory: rising supply, slower turnover, and a gradual return to balance after an elongated correction cycle.

None of these changes appear temporary. The expansion of inventory reflects a structural shift toward normalization, where buyers benefit from more choice and more time. Sellers, in turn, must price with precision, present homes competitively, and avoid strategies based on momentum that no longer exists in today’s market.

Pricing Trends and Market Direction

Prices across the Austin-Area MLS remain stable, but the growth pattern has flattened compared with prior years. The average active list price increased modestly from $563,757 to $576,064, up 2.2% year over year. The median active list price declined from $439,925 to $435,000, a -1.1% shift that reflects a market leaning toward mid-range inventory rather than luxury-heavy listings. This subtle divergence between average and median prices points to a pricing environment that is holding steady rather than accelerating.

Sales data reinforces this picture of moderation. The average sold price increased from $543,807 to $554,285, a 1.9% year-over-year gain. The median sold price declined slightly from $425,250 to $422,000, down -0.8%. Inside the City of Austin, downward adjustments are more pronounced. The average active list price fell from $791,408 to $746,012, down -5.7% year over year, while the median active list price dipped -1.7% to $575,000. Sales followed the same pattern, with the average sold price dropping -5.7% to $716,663 and the median sold price declining -2.6% to $560,000.

Directionally, the pricing structure is stable but clearly not in an appreciation cycle. Buyers remain highly value-focused, and sellers who push prices above market alignment see extended days on market and deeper concessions. This is a discipline-first environment where strategy matters more than speed.

Negotiation Environment and Buyer Leverage

Negotiation patterns continue to favor buyers across the Austin-Area MLS. So far this month, 68.89% of all sold properties have closed below the list price, compared with 70.89% last month. Another 19.22% closed at list price, while 11.88% sold above list—up slightly from 10.92% last month and well above the 9.97% level seen in November 2024. Even with the small increase in over-ask closings, the larger trend remains clear: this is still a market where buyers dictate terms more often than sellers.

The average sold-to-list price ratio currently stands at 96.94%, confirming that sellers are conceding roughly 3% from list on average. While concessions remain consistent, they have stabilized, suggesting that sellers who price accurately can still secure clean offers. Mispriced listings, however, take longer to move and often require price reductions to realign with market expectations.

Precision is now the competitive edge. Buyers gain leverage through expanded selection and lower urgency, while sellers win when their list price reflects real comparables, not aspirational targets.

Regional & ZIP Code Performance

Market performance across Central Texas remains mixed but balanced. Month over month, 19 of 30 tracked cities (63%) reported price increases, while 11 (37%) posted declines. Year-over-year results show a similar distribution, with 14 cities (47%) gaining and 16 (53%) declining. Notably, none of the 30 cities remain above their 12-month peak; all 30 are below peak levels, confirming a full normalization cycle.

Across 75 ZIP codes, 41 (55%) posted month-over-month price increases, while 33 (44%) saw declines. Year over year, 39 ZIP codes (52%) are up and 36 (48%) are down—another sign of balanced market behavior rather than broad directional momentum. Only one ZIP code in Central Texas is above its 12-month peak, while 74 remain below, reflecting the same post-correction stability observed at the city level.

Market variance is now driven by hyperlocal factors: affordability, school district preference, product type, and neighborhood demand cycles. The broader regional trend is no longer declining—it is stabilizing.

Prices Relative to Peak Levels

Relative to peak conditions, the market has fully corrected and is now holding steady. In the Austin-Area MLS, the average sold price is 17.3% below its May 2022 peak, while the median sold price is down 21.9%. Price per square foot is 25–26% below peak levels, consistent with the broader correction observed over the past two years.

Inside the City of Austin, the pullback is similar. Median sold price is 17.3% below the May 2022 high, and the average sold price is down 15.7%. Price per square foot is down between 25% and 28%, depending on average vs. median. These declines are structural, not temporary. The correction is complete, and the market is now operating within a stable post-peak range.

Market Outlook

As we move into late 2025, the Austin housing market is transitioning into a steady and predictable phase after a multi-year correction. Supply continues to expand at double-digit rates, yet pricing remains stable, and appropriately calibrated listings still find buyers. Over-ask activity is rising slightly but remains limited to segments where inventory is tight and product alignment is strong.

The outlook is clear: buyers retain control over timing and negotiation, while sellers succeed through accuracy, readiness, and realistic pricing. Momentum is no longer the driving force—value justification is. Austin has shifted out of volatility and into a balanced, post-correction cycle that sets the stage for a more predictable 2026.